Table of Contents

The Bottleneck Nobody’s Talking About: Financing EV Freight in India

What will it really take to put zero-emission trucks on India’s highways, and who will pay for the infrastructure to charge them?

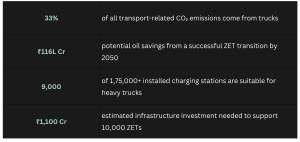

India has 175,000 electric charging stations but only 9,000 of them can actually charge a truck. This single fact captures the scale of the challenge ahead. This gap is not just a logistical constraint, it directly shapes India’s ability to decarbonise its freight sector, one of the hardest segments to transition.

Climate change is no longer a distant threat, and how India manages its transportation sector will be one of the most consequential decisions it makes as a country. The least-developed nations, responsible for just 3% of global emissions, are bearing the steepest consequences, and India sits squarely in this crossfire.

The session, part of the Harris Lecture Series, was led by Nikita Bankoti, co-author of RMI’s landmark July 2025 report, Financing Zero-Emission Trucking Infrastructure in India. Her lecture titled “Mitigating Climate Risk: Unlocking Climate Finance for Hard-to-Abate Transport Sectors” was both a masterclass in policy design and a brutally honest accounting of just how far India has to go.

KEY NUMBERS AT A GLANCE

Why Trucks? Why Now?

Trucks represent just 3% of vehicles on Indian roads. Yet they are responsible for more than half of all particulate matter emissions from transport and one-third of transport-related CO₂. As e-commerce explodes and road freight is projected to grow fivefold, this problem is not static, but compounding. The sector is one of the fastest-growing contributors to India’s carbon footprint, and one of the hardest to decarbonise.

Zero-emission trucks (ZETs) offer a genuine way out. A successful transition could eliminate NOx and particulate tailpipe emissions, reduce cumulative carbon output by 2.8 – 3.8 gigatonnes by 2050, and unlock an estimated ₹116 lakh crore in oil savings. That is not a marginal gain, it is a structural transformation of India’s energy economy.

The Charging Infrastructure Problem

The central insight of Nikita’s lecture was deceptively simple: zero-emission trucks are only as good as the infrastructure that charges them. And right now, India does not have that infrastructure. Of more than 175,000 charging stations currently installed across the country, only around 9,000 are capable of meeting the high-power demands of heavy-duty trucks.

This creates a classic chicken-and-egg problem. Truck manufacturers are ready to build ZETs. Fleet operators are watching the market. But without charging stations, there is no confidence to make the switch. And without trucks on the road, there is no revenue to justify building the charging stations. As Nikita put it: “the bottleneck here is not technology; it is finance, coordination, and trust.”

Each of these deserves an unpacking.

Finance is the most visible barrier. ZET infrastructure requires significant upfront capital, but the returns are slow and uncertain, especially when truck utilisation on electric vehicles is still low. Private investors are hesitant to move first. This is precisely why public and blended financing mechanisms need to step in and de-risk early investments, creating the conditions for private capital to follow.

Coordination is the less obvious but equally critical challenge. Charging infrastructure cannot be built randomly, it needs to align with freight corridors, grid capacity, land availability, and fleet operator schedules. Without active coordination between government agencies, power utilities, logistics companies, and financiers, even well-funded projects can stall. No single player can solve this alone.

Trust may be the hardest to build. Small fleet operators, who make up the majority of India’s trucking sector have little margin for error. Asking them to switch to a technology that is new, expensive, and dependent on infrastructure that does not yet exist is asking them to take a leap of faith. That trust is only built through demonstrated pilots, transparent data, and consistent policy signals over time.

Until all three are addressed together, the transition will remain stuck, not for lack of ambition, but for lack of alignment.

Who Will Pay and how?

This is where the lecture became genuinely exciting from a policy perspective. Nikita walked us through the four primary financial tools that can unlock this transition: debt, equity, government fiscal tools, and blended finance.

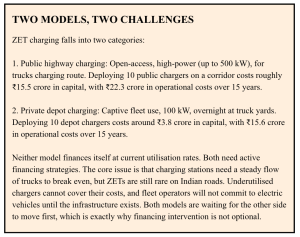

The key insight here is that no single instrument works alone, and different instruments suit different types of charging. Public charging stations, which function as quasi-public goods, need government support to bridge the gap between high upfront capital and slow, uncertain revenue. Private depot charging, with its captive fleets and predictable utilisation, is better suited to market-based financing once lenders are sufficiently de-risked.

Each tool has a distinct role. Debt, through commercial loans and credit lines is the most familiar, but traditional lenders remain cautious in a nascent market with no long track record. Equity, both concessional and private, can absorb early-stage risk that lenders will not take on. Government fiscal tools like capital subsidies and viability gap funding make the economics viable in the early years without replacing private finance entirely. Lastly, ‘Blended Finance’ then brings all of this together by using a small amount of public money to reduce risk just enough for private capital to follow.

The SIDBI Risk-Sharing Facility, co-funded with the Shell Foundation, offers one promising example already in operation: a ₹50 crore facility using a partial credit guarantee to encourage NBFCs to lend to charge point operators (CPOs). It projects a 14x capital leverage effect, meaning every ₹1 of public money is expected to mobilise ₹14 in private investment. The government does not need to fund the entire transition. It needs to take on enough risk to convince private investors the market is viable, and a well-targeted public commitment can do exactly that. In my understanding, this is exactly the kind of catalytic structure that can move a market before it is ready to move on its own.

The Delhi-Jaipur highway corridor was cited throughout the lecture as an ideal test case. A high-volume freight route with demonstrated demand, it could serve as proof-of-concept for both public charging and the Charging-as-a-Service (CaaS) model, where a CPO owns and operates depot infrastructure for a fixed fee, shifting risk away from fleet operators entirely.

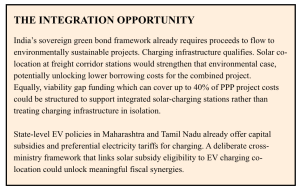

A Question Worth Asking: Can Solar Subsidies Do Double Duty?

ZET charging stations along freight highways face two simultaneous financial burdens: high grid infrastructure costs and high electricity tariff costs. Grid upgrades to support the 500 kW loads of public charging stations can alone exceed ₹8 crore per site. Electricity costs, over a 15-year project life, represent the single largest share of total ownership costs. Both problems improve meaningfully if the charging site co-locates with solar generation.

This raised a question in my mind during the session: India is already spending significant public money subsidising rooftop and utility-scale solar installations. Could that fiscal infrastructure be intelligently integrated with EV freight corridor development to reduce the cost of public charging?

The answer is – carefully, but yes. It is not a wrong instinct, but it is not a simple integration either. The challenge is coordination. Solar subsidies sit with one set of ministries, EV infrastructure with another, and freight corridor planning with yet another. Making them work together requires aligning incentives, timelines, and approvals across multiple stakeholders, something India’s policy architecture is not yet set up to do smoothly. The synergy is real, but unlocking it is as much a governance challenge as a financial one.

There are real complications to navigate. Solar generation is intermittent; a 500-kW charging load is large and demand-spiked. On-site solar alone cannot power a highway truck stop. Grid connectivity remains essential. But as a supplementary cost-reducer funded in part through existing solar subsidy channels- the idea is not only financially sound, it is potentially transformative for the viability of public charging along India’s freight corridors.

More importantly, this kind of cross-sector thinking asking whether solar policy and EV policy can reinforce each other rather than operating in separate ministry silos is precisely what India needs more of. Climate finance works best when it compounds.

What I Took Away

Nikita’s lecture reminded us that climate finance is not abstract. It is deeply structural. It is about who bears risk, who captures revenue, and how public and private actors coordinate in a market that does not yet exist at scale. The chicken-and-egg problem of charging infrastructure is ultimately a coordination failure, not a technology failure or even a capital failure. The money exists. The technology exists. What is needed is a coherent set of instruments, deployed in sequence, to build market confidence until private capital can sustain the transition on its own.

India has set 10,000 ZETs on the road as a near-term strategic target. Achieving that milestone, RMI estimates, requires roughly ₹1,100 crore in charging infrastructure investment. That is achievable. But it requires governments to stop treating charging infrastructure as a downstream consequence of EV adoption and start treating it as a prerequisite something that must be built ahead of, or alongside, the trucks themselves.

“Your net worth is your network” and in the case of zero-emission freight, India’s climate net worth may well depend on the charging network it builds today.

At ISPP, we are learning to ask not just what policy is needed, but who finances it, who implements it, and who bears the risk when it fails. Nikita’s session gave us a masterclass in exactly that, and sent me back to the reading with a renewed sense of urgency about one of India’s most important decarbonisation challenges.

References:

Nikita Bankoti et al., Financing Zero-Emission Trucking Infrastructure in India, RMI, July 2025. https://rmi.org/insight/financing-zero-emission-trucking-infrastructure-in-india

Nikita Bankoti, Guest Lecture at ISPP, February 2026.